M&A activity highlights the value disconnect.

Maxam Diversified Strategies – Q3 2023 Commentary

Dear fellow investors,

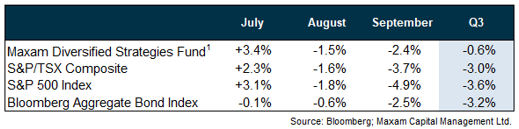

The Maxam Diversified Strategies Fund1 declined -0.6% in the third quarter of 2023.

Q3 was a difficult quarter for both equity and bond markets. After a positive start to the quarter, the now all-too-familiar market narratives of high inflation, rising interest rates, recession fears and geopolitical conflicts began to dominate again. If that wasn’t enough, late August through early October is often the weakest seasonal period for equities each year.

As we finish the weakest seasonal period of the year, we enter the strongest seasonal period through year-end. A year-end rally would be very welcome of course – but whatever transpires it seems appropriate to expect continued market volatility in the near term.

You know those Buffett quotes that everyone loves?

The wall of worry is steep today. It is understandable, there is a lot to worry about with respect to the capital markets, the economy, and the world. And worry brings opportunity – companies are not cheap when everything is rosy and reflected in stock prices.

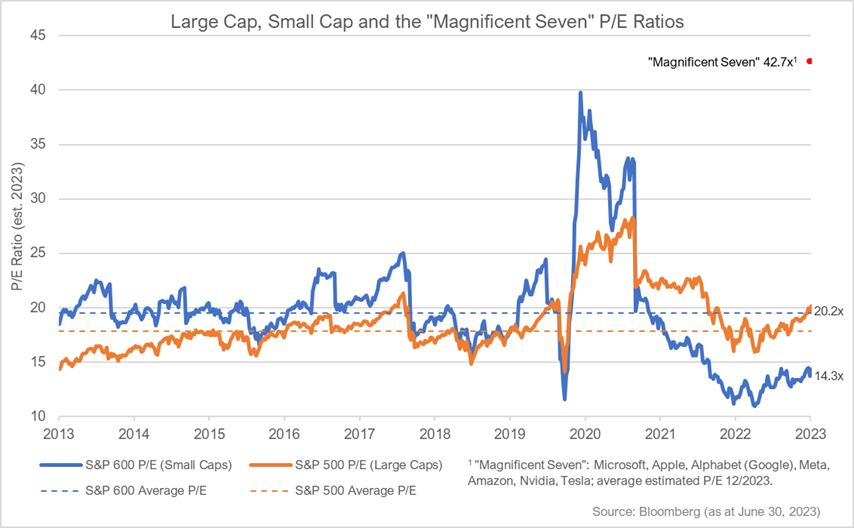

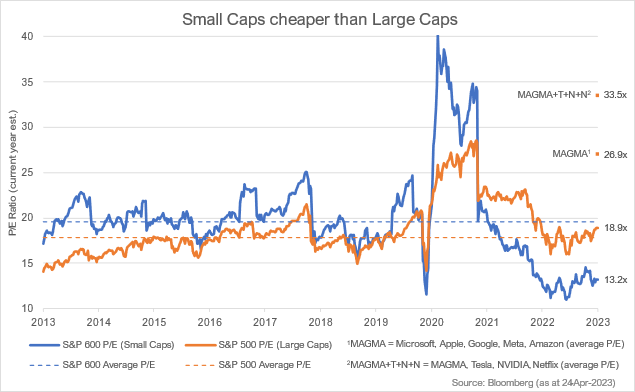

Framing part of the opportunity set: it has been a terrible market for small and mid-cap stocks over the last couple of years. The Russell 2000, S&P 600, and S&P/TSX Small Cap are down -31%, -25% and -23% since November 20212.

And it’s not just small and mid-caps. The S&P 500 Equal Weight Index is down -15% over that same time frame2. In our Q1 and Q2 commentaries we discussed the narrow breadth of the market this year and how a few mega cap companies were masking the weakness and opportunity beneath the surface.

Like a broken record, we have also been highlighting that small and mid-cap securities currently trade at a material valuation discount to large caps. Small caps have historically traded at a valuation premium to large caps, but they have shifted to a discount because as a group they are perceived to be more sensitive to the economy, inflation, and interest rates.

A recession may be a matter of ‘when’ not ‘if’ at this point – in any event, we see one already reflected in many security prices today. History reveals that markets are forward discounting mechanisms – and small caps typically outperform as inflation declines, interest rates fall, and the economy troughs and exits a recession.

Today we have an environment characterized by fear and an opportunity set full of securities that are down materially from their highs, trading at attractive valuations.

Take advantage. Be greedy when others are fearful.

There must be something in the water.

We have mentioned our investment in water infrastructure and technology company H2O Innovation in our quarterly commentaries on five previous occasions. On four instances we noted that it was a positive contributor to performance, and once that it was a negative contributor.

In our Q2 2022 commentary, when H2O was a detractor from performance, we wrote:

We’ve recently added to our position in H20 Innovation Inc., a water infrastructure and technology company whose shares were down -32% through the first six months of this year. We like this founder led business that has highly recurring revenues and is delivering strong organic and acquisitive growth.

Our intention was to highlight that we were adding to a high-quality and growing business that was trading at what we thought was an unreasonably depressed share price. And in our most recent commentary – yes just a few months ago – we took a small victory lap when H2O’s shares, reflecting the strong performance of the business, performed quite well.

Fast forward to the quarter that just finished on September 30th: H2O’s share price declined from $3.20 to $2.61, down -18%. Stock prices are volatile – often much more so than their underlying businesses.

We were preparing to write about the opportunity to add to this quality business again… H2O was performing quite well but getting no love from investors – albeit in a very difficult market environment, particularly for stocks not named NVIDIA or associated with the recent AI mania3.

On October 3rd H2O announced that they had entered into a definitive agreement to be acquired by Ember Infrastructure Management, a New York-based private equity firm, for $4.25 cash per share – a significant premium to where the public market was valuing the business.

Beyond H2O being a successful investment for the fund, it is illustrative of the value disconnect that exists for select companies in this market environment, and the opportunity that exists for investors.

With many quality small and mid-cap companies trading at unreasonably low valuations, or material discounts to their larger peers, we expect to see an uptick in M&A activity. Either the market will provide deserving businesses with a reasonable valuation, or an opportunistic acquiror will.

Exposures.

At the end of the third quarter the fund was well diversified across 11 industry sectors and its top 25 positions accounted for approximately 51% of net assets. From a strategy perspective, fund exposures include 66% in fundamental longs, 28% in special situations, 4% in convertible debentures, 12% in arbitrage, and approximately 2% gross exposure in short positions.

Positive contributors to fund performance during Q3 included Vitalhub, Celestica, NexGen Energy, Sprott Physical Uranium Trust and AG Growth International. Some notable detractors from performance in the quarter included H2O Innovation, Calian Group and Hamilton Thorne.

We have more value and catalyst rich names like H2O Innovation in the fund today.

Redux

There is compelling value beneath the surface of the mega cap companies that have garnered the preponderance of investor attention this year. Looking beyond any near-term volatility I see one of the best set ups for our style and approach since 2000 and 2009.

In 2000 the internet and technology bubble was bursting, former darlings declined and previously ignored companies and segments of the market began a period of significant outperformance.

In 2009, fears of ongoing recession following the GFC4 lingered in the psyche of investors, paralyzing them from action. But valuations were very attractive on normalized results – especially in quality small and mid-caps – creating a favourable environment for active investors.

Compounding our experience and learned knowledge, we see many of those same market dynamics present today.

Step up to the plate.

We concluded our last commentary with a section titled the “Hitter’s count” – describing the positive set up we see for deploying capital. With many security prices down significantly over the last couple of years that set up is increasingly attractive today.

Taking advantage of fear does not mean we aren’t mindful of the present risks – but it is precisely because investors are focused on those risks that we find ourselves in this fertile investment environment.

Looking through any near-term market volatility we see strong performance coming from the companies we own materially re-rating, targeted catalysts occurring, and/or a wave of M&A as opportunistic acquirers step in to take advantage of significant value dislocations.

Thank you for your trust, patience, and confidence. Please don’t hesitate to reach out with any questions.

Sincerely,

Travis Dowle, CFA

President & Fund Manager

Maxam Capital Management Ltd.

1 Maxam Diversified Strategies Fund, Series F, net of fees and expenses. Please contact us regarding other classes of fund units or visit our website www.maxamcm.com. S&P/TSX Composite, S&P 500 Index and Bloomberg Aggregate Bond Index data sourced from Bloomberg.

2 Index performance data sourced from Bloomberg.

3 While AI is a legitimate growth area and opportunity for many businesses, the hype has created some inflated valuations. NVIDIA is a great company, but it might not trade at a great valuation today. Here’s an infamous quote from Scott McNeely, former CEO of Sun Microsystems, describing his company’s valuation during the technology and internet bubble that burst in 2000:

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

4 GFC is the acronym for the Great Financial Crisis circa. 2007-2008. https://en.wikipedia.org/wiki/2007–2008_financial_crisis

This information is intended to provide you with information about the Maxam Diversified Strategies Fund and is not an offer to sell or solicit. Disclosed performance is based on Class X, A and F units and is net of all fees and expenses. Inception date for Class X is June 30, 2009; Class A is December 31, 2012 and; Class F is January 31, 2013. The performance fees on Class X units are subject to a 5% annualized hurdle. Important information about the Fund is contained in the Simplified Prospectus and Fund Facts which should be read carefully before investing. Prior to August 24, 2022 this Fund was offered via Offering Memorandum only and was not a reporting issuer. Historical audited financial statements for this period are archived here. The expenses of the Fund would have been higher during such period had the Fund been subject to the additional regulatory requirements applicable to a reporting issuer. Prior to becoming a reporting issuer, the Fund was not subject to the investment restrictions and practices in NI 81-102. Important information about the Fund is contained in the Fund’s Simplified Prospectus, which should be read before investing. This presentation is neither an offer to sell securities nor a solicitation to sell securities. The securities of the Fund are sold only through IIROC registered dealers in those jurisdictions where it may be lawfully offered for sale. Accredited investors or certain other qualified investors may also purchase securities through Maxam Capital Management Ltd in reliance on certain prospectus exemptions available in National Instrument 45-106. Investors should consult with their own investment advisor and obtain a copy of our applicable Simplified Prospectus and Fund Facts documents before investing in the Fund. Investors should seek advice on the risks of investing in the Fund before investing. This document may contain forward-looking statements. These forward-looking statements are based upon the reasonable beliefs of Maxam Capital Management Ltd. at the time they are made and are not guarantees of future performance, are subject to numerous assumptions, and involve risks and uncertainties about general economic factors which may change over time. Maxam assumes no duty, and does not undertake, to update any forward-looking statement and cautions you not to place undue reliance on these statements as actual events or results may differ materially from those expressed or implied in any forward-looking statements made. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the Simplified Prospectus before investing. Any indicated rates of return are the historical annual total returns including changes in value and reinvestment of all distributions and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. This document is not intended to provide legal, accounting, tax or investment advice. Please consult an investment advisor and read the prospectus for the Maxam Diversified Strategies Fund prior to investing.